GOVERNMENT OF THE PUNJAB

LOCAL GOVERNMENT AND COMMUNITY

DEVELOPMENT DEPRTMENT

February 07, 2017

NOTIFICATION

No.SOR(LG)38-19/2016. In exercise of the powers conferred under section 144 of the Punjab Local Government Act 2013 (XVIII of 2013) and after previous publication, Governor of the Punjab is pleased to make the following rules:

PART-I

Preliminary

1. Short title, commencement and application.- (1) These rules may be cited as the Punjab Union councils (Accounts) Rules 2017.

(2) They shall come into force at once.

2. Definitions.- (1) In these rules:

(a) “Act” means the Punjab Local Government Act 2013 (XVIII of 2013);

(b) “audit and inspection report” means the report of the Auditor General of Pakistan containing audit observations related to the accounts of the union council;

(c) “audit para” means the report of the Auditor General, Pakistan submitted to Governor of the Punjab under Article 171 of the Constitution of Islamic Republic of Pakistan to be laid before Provincial Assembly of the Punjab;

(d) “audit report” means a report of the Auditor General of Pakistan containing draft (printed) audit paras to be considered by the Public Accounts Committee;

(e) “bank” means any scheduled bank approved by the Government;

(f) “Chairman” means the Chairman of the union council;

(g) “current expenditure” means the expenditure other than the development expenditure;

(h) “Departmental Accounts Committee” means a committee of the Local Government and Community Development Department of the Government, consisting of Secretary of that department or his nominee as Convener, Secretary of the union council and a representative of Audit as members to consider and settle audit observations contained in the audit and inspection report pertaining to the accounts of the union council and any other matter referred to it by the Public Accounts Committee or Punjab Local Government Commission or the Government;

(i) “development expenditure” means an expenditure on development projects or an expenditure on new construction, new works or additions and alterations to existing works or repairs of the newly purchased or previously abandoned buildings and works;

(j) “drawing and disbursing officer” means the Chairman for purposes of Incurring expenditure and to making disbursement of the account so withdrawn in respect of the union council;

(k) “financial irregularity” means the financial irregularity as defined in para 13.7 of Chapter 16 of Punjab Budget Manual and includes:

(i) the expenditure Incurred without sanction;

(ii) the expenditure incurred without sufficient appropriation or without proper justification;

(iii) extravagance or wastage of the local fund;

(iv) loss of the union council money or property owing to misappropriation; fraud, negligence or

(v) over budgeting or under budgeting; and

(vi) breach of the Act or the rules.

(l) “Forms” means the Form appended to the rules;

(m) “House” means the elected body of the union council;

(n) “new accounting model” means the model prescribed by Auditor General of Pakistan in terms of clause (1) of Article 170 of the Constitution of the Islamic Republic of Pakistan, 1973 and includes, the accounting format, forms, principles of chart of accounts, accounting policies, procedures Manual (APPM) and APPM book of Forms and any other material relating thereto;

(o) “principal accounting officer” means the Chairman of a union council, responsible for the preparation of the budget of receipts and expenditure, collection of revenues, utilization of the budget and maintenance of departmental accounts in the prescribed manner” and is accountable to the Public Accounts Committee in respect of financial and budgetary matters of the union council;

(n) “public account” means other monles, including pension contribution, tax deductions, securities and other receipts by the union council on behalf of the other parties as trust for a special purpose and not available for appropriation;

(p) “Public Accounts Committee” means the Committee of Provincial Assembly of the Punjab for consideration of the audit report on the accounts of union council;

(q) “rules” means the Punjab Union Councils (Accounts) Rules 2017;

(r) “Special Departmental Accounts Committee” means a committee of Local Government and Community Development Department of the Government, consisting of the Secretary of that department-or his nominee as convener, the Chairman of the union council and a representative of the concerned Director General Audit as members to consider and settle advance audit paras and proposed draft paras pertaining to the accounts of the union council or any other matter referred to it by the Public Accounts Committee or Punjab Local Government Commission or the Government; and

(s) “union secretary” means the Secretary (Community Development) of the union council.

(2) A word or expression used but not defined in the rules shall have the same meaning as is assigned to it in the Act.

PART-II

Local Fund, Bank Account and Forms

3. Custody and operation of the local fund and public account. (1) The local fund and public account of the union council shall be kept in the bank, as far as possible, at the headquarter of the union council.

(2) The local fund and public account of the union council shall be kept in separate bank accounts.

(3) The union council may, and if required by Government, shall maintain a separate bank account for any special purpose but it shall be maintained, administered and regulated as if it were the local fund.

(4) The funds will lapse on 30th June of the financial year and the balance available on 30th June of that year shall be deposited in the respective receipts head of account of the union council.

(5) No expenditure shall be incurred except against the budget of that year.

(6) The union council may, and if required by Government shall, maintain a separate development fund.

(7) The bank accounts of the local fund and public account of the union council shall be jointly operated by the Chairman and the Union Secretary.

4. Mode of payment.- (1) The mode of payment from local fund shall be that:

(a) payments up to five thousand may be made by any means;

(b) payments exceeding rupees five thousand shall be made through crossed non-negotiable cheque; and

(c) the cheque shall be personally collected by the payee or his authorized agent.

(2) In case, a cheque is not received by the payee or is lost or stolen, the notice to stop payment shall be given by the Chairman to the concerned bank.

(3) A replacement cheque shall be issued to the concerned payee only on receipt of the acknowledgement for non-payment from the bank.

(4) If a cheque is not claimed or presented and paid within the due date or up to 30th June of the financial year, it shall be a stale cheque and a new cheque shall only be issued on the deposit of stale cheque with the drawing and disbursing officer.

(5) A cheque book shall be kept in the safe custody of the Union Secretary.

5. Maintenance of accounts.- Subject to the provisions of the Act, the accounts of the receipts and expenditures of the union council shall be maintained in such form and in accordance with such principles and methods as are given in the new accounting model:

(a) the accounts of the union council shall be maintained on single entry system;

(b) all transactions in the accounts of the union council shall be cash based and not accrual based;

(c) the accounts shall be maintained in English or Urdu language as the House may determine;

(d) the English system of numeration shall be adopted;

(e) all cash shall be in Pakistani rupees;

(f) any sum payable to the union council shall be paid in cash or through pay order or bank draft;

(g) all receipts of the union council shall be collected through the bank but, in rare cases and if so resolved by the House, the receipt may be collected in cash in the prescribed manner;

(h) all cash transactions shall be entered in the receipts register and general cash book and the entries shall be verified;

(i) the record relating to the accounts shall be clear, explicit and self-contained, and no erasure or overwriting shall be made in any accounts register, book or form, and the correction, if required, shall be made, in red ink with date and initials of the Union Secretary;

(j) the payment of approved claims shall be made only to the claimant as mentioned in the claim voucher;

(k) the expenditure shall not be set off against the receipt and no expenditure shall be made from any receipt by the union council; and

(l) all expenditures shall be recorded on gross basis against relevant appropriation.

6. Forms. (1) The accounts of the union council shall be maintained in the Forms or as prescribed by Auditor General of Pakistan.

(2) All Forms shall be machine numbered, printed by the Government Printing Press and kept in the personal custody of the Union Secretary.

PART-III

Responsibilities of the Functionaries

7. General.- In case of any loss to the local government through fraud or negligence:

(a) the person functioning on behalf of the union council shall be personally responsible and shall be liable to make good the loss;

(b) the drawing and disbursing officer and payee of the pay, allowances, contingent expenditure or any other expense shall be personally responsible for any overcharge, fraud or misappropriation and shall be liable to make good that loss; and

(c) a collector of tax, fee, rate, charge, surcharge of the Union council shall be personally responsible for any overcharge, fraud, misappropriation or any unnecessary delay in crediting the amounts so collected to the account of the union council and shall be liable to make good the loss arising from his culpable negligence.

8. Responsibilities of the Chairman.- (1) The Chairman shall

(a) the principal accounting officer of the union council;

(b) accountable to the Public Accounts Committee;

(c) responsible for maintenance of accounts and financial discipline in the union council; and

(d) responsible for compliance of the directions of the Public Accounts Committee.

(2) In the discharge of his responsibilities, the Chairman shall ensure that:

(a) the accounts of the union council are maintained correctly and efficiently;

(b) the annual accounts of the union council are countersigned by the Chairman and sent to the Government by 15th July of each year;

(c) the internal controls and management of the funds and expenditure are on ground;

(d) any sums due to the union council are promptly realized and credited to the local fund;

(e) the amount credited to local fund, as reported by the Union Secretary, are reconciled and verified with the record on monthly and annual basis;

(f) the procedures for generation, control and evaluation of bills and demand notices required under rules are followed; and

(g) the participation in the meetings of the Departmental Accounts Committee, Special Departmental Accounts Committee and Public Accounts Committee..

9. Responsibilities of the Union Secretary. (1) The Union Secretary shall be responsible to:

(a) prepare the estimates of receipts;

(b) make assessment of tax, fee, rate, charge and other levies of the union council on periodical and annual basis;

(c) maintain demand and collection register of income;

(d) collect the receipts of the union council in a transparent manner;

(e) cause to credit the amount collected against any demand to the local fund bank account and record necessary entries in the demand and collection register, cash collection register and other relevant books of accounts;

(f) prepare monthly and annual statements of receipts and reconcile the statements with the bank;

(g) submit monthly and annual receipts accounts to the Chairman for countersignature;

(h) prepare statement of arrears at the beginning of each financial year by carrying forward and include the same in the demand of the following financial year; and

(i) attend to the audit and inspection reports of receipts and promptly prepare annotation to observations.

(2) The Union Secretary shall:

(a) prepare estimates of expenditure;

(b) maintain budget control register of expenditure and make assessment of expenditure on periodical and annual basis;

(c) withdraw and disburse monies from the local fund in a transparent manner;

(d) maintain cash book and promptly record entries in the cashbook as soon as the amount is withdrawn, disbursed or credited to the local fund or public account; and

(e) prepare monthly and annual statements of expenditure and reconcile the statements with the bank.

(3) The Union Secretary shall:

(a) maintain day-to-day accounts of the union council;

(b) perform pre-audit of all payments from the local fund and public account of the union council before authorizing disbursement of the amount;

(c) operate the bank accounts of the union council Jointly with the Chairman;

(d) prepare monthly and annual statement of receipts and expenditure; and

(e) transmit the annual statement of accounts of the union council for the preceding financial year to the House and the Government through the Chairman by 15th July each year.

10. Relationship with the bank.- (1) The Union Secretary shall interact with the bank for the receipts, payment and reconciliation of cash.

(2) The Union Secretary shall obtain the following returns from the bank on daily basis:

(a) bank scroll;

(b) paid cheques;

(c) receipts paid challan; and

(d) transfer advices.

PART-IV

Receipts

11. Mode of collection of receipts. (1) Except as provided in sub-rule (2):

(a) all receipts of the union council shall be collected through the bank;

(b) all sums due to the union council shall be paid in cash or through a bank draft or pay order;

(c) all receipts shall be classified in accordance with the Chart of Accounts! specifications;

(d) all amounts to be deposited in the bank shall be accompanied by a receipt paid challan; and

(e) the revenue shall be recognized in the books of accounts on the basis of the receipts and paid challans verified through the bank scroll after the money is actually received at the bank.

(2) In exceptional cases and if so resolved by the House, any receipts may be collected in cash but the Union Secretary shall be personally accountable for the amount received in cash and shall maintain a proper record of the receipts.

(3) All cash or bank drafts or pay orders received at the office of the union council shall be acknowledged in Form-AR5.

(4) All receipts shall be written in figures and words with copying pencil in duplicate by carbon process and the carbon copy shall be retained by the Union Secretary issuing the receipt and the original shall be handed over to the person making the payment;

(5) All receipts shall be personally signed by the Union Secretary.

(6) A duplicate copy of the receipt shall not be issued but, if necessary, a certificate may be given indicating the particulars of receipts.

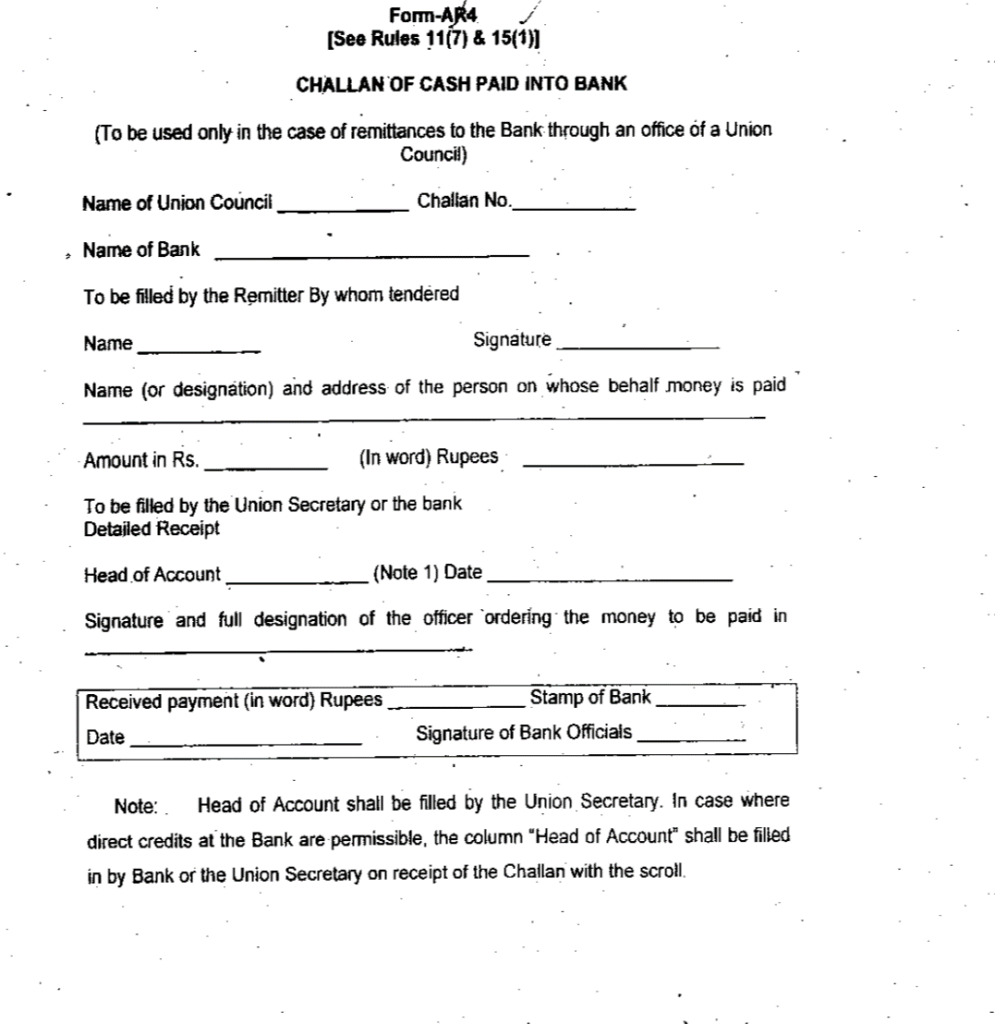

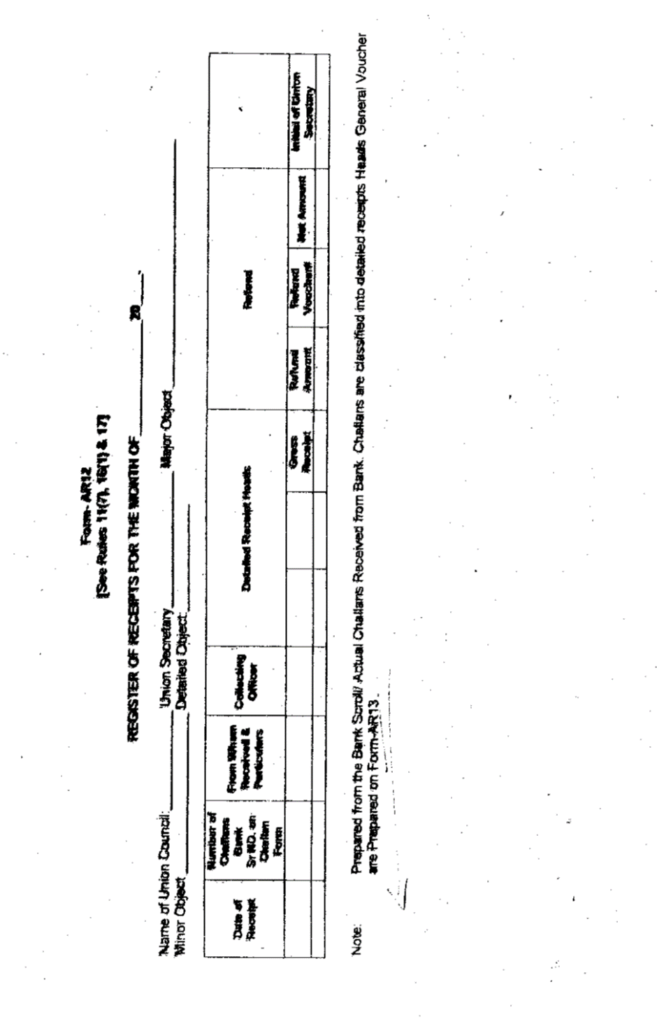

(7) The Union Secretary shall deposit, on dally basis, all receipts collected in cash in the bank account on the bank challan in Form-AR4 and shall invariably enter the receipts in the register of receipts in Form-AR12.

12. Receipt books. All receipt books shall be kept in following manner:

(a) all receipt books shall be machine numbered and shall be kept in the personal custody of the Union Secretary;

(b) the number of receipt forms contained in each receipt book shall be counted and recorded in the book at a conspicuous place under the signature of the Union Secretary;

(c) when all receipts in a receipt book have been used, the Union Secretary shall record a certificate on the used receipt book that all the receipts through the receipt book have been duly credited in the bank account of the union council and duly verified; and

(d) the used receipt books shall be kept in the personal custody of the Union Secretary for record, annual audit and inspection.

13. Levies. A tax, fee, toll, cess, charge, rate or any other levy shall be effective only after the appropriate notification is published in the official Gazette.

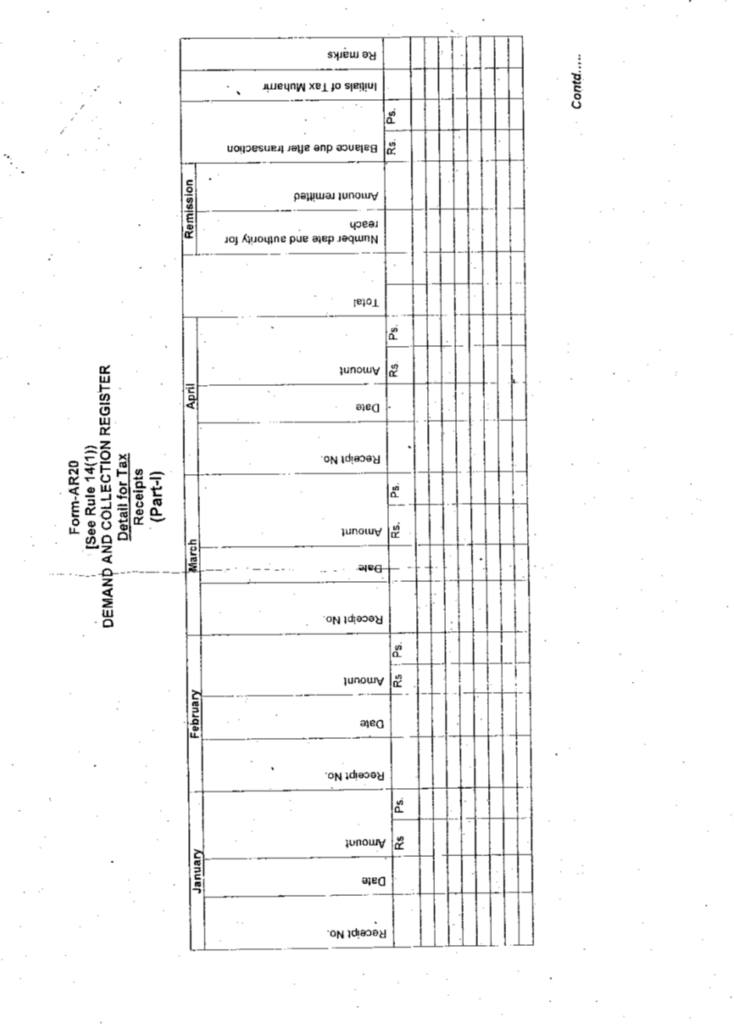

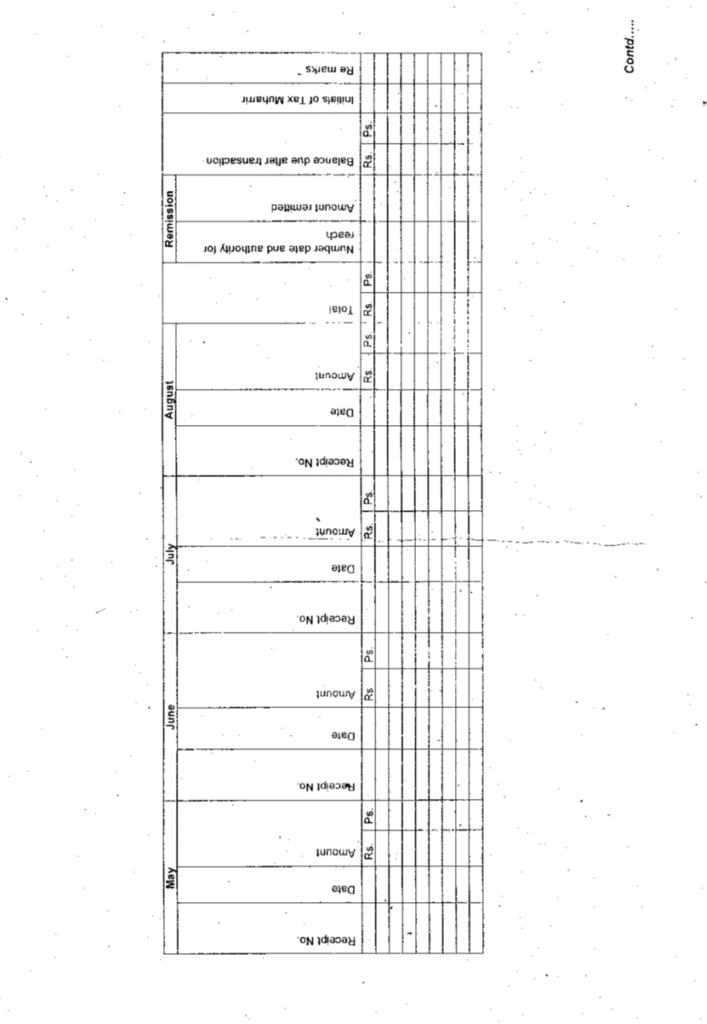

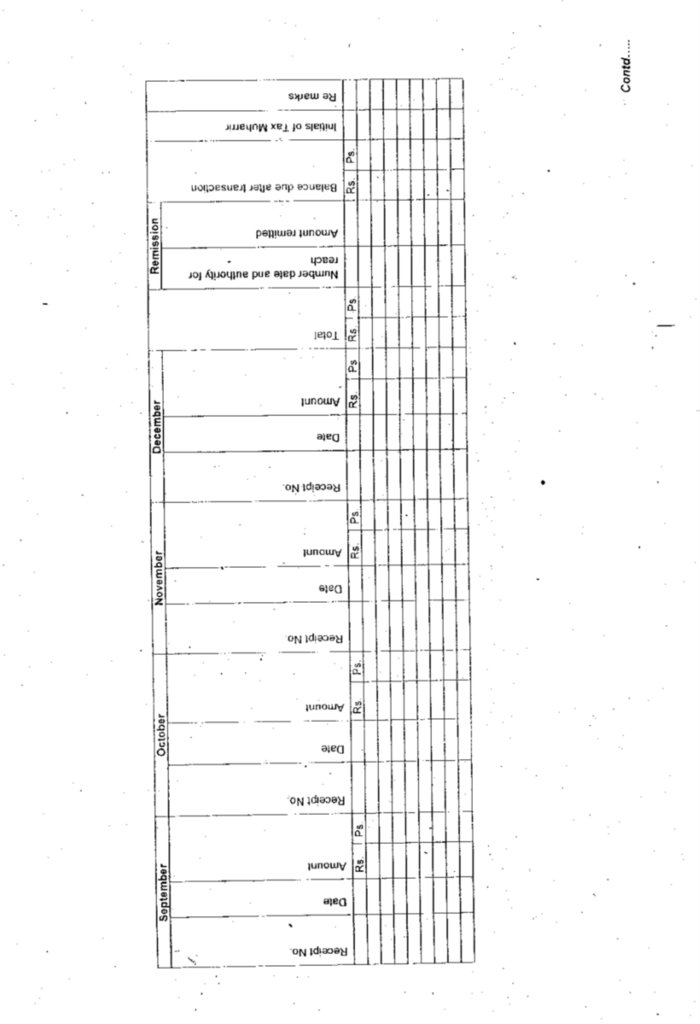

14. Demand and collection register.- (1) A demand and collection register shall be maintained by the Union Secretary in Form- AR20.

(2) Where a Union council levles a tax, rate, fee or any other charge for which periodical assessment is necessary, the demand shall be raised after the assessment is approved by the Chairman but in other cases, the demand shall be raised in the beginning of a financial year.

(3) The money received against any demand shall be entered in the demand and collection register.

(4) At the end of every month, a statement showing progress of the demand and collection shall be prepared, reconciled with the bank and submitted to the Chairman.

(5) At the beginning of each year, the arrears of the previous year shall be carried forward and included in the demand for the following financial year.

(6) The aggregate of monthly and annual total recoveries as per demand and collection register shall be reconciled with the corresponding figures in the classified Abstract, within one week of the close of relevant month and year in Form-AR19.

15. Receipt of money by bank.- (1) Three coples of the bank challan in Form-AR4 shall be prepared by the Union Secretary under his signature and shall contain complete particulars of the receipt.

(2) The bank, on receiving the receipts in cash or through bank draft or pay order shall stamp the receipt challan and distribute the copies in following manner:

(a) original copy shall be given to the payee;

(b) the second copy shall be sent to the Union Secretary; and

(c) third copy shall be retained by the bank.

(3) The Union Secretary shall keep the challan copy for maintenance of his record.

(4) No additional copies of receipt challan shall be provided to any person but in case the original paid bank challan is lost, a letter under the signature of the Chairman may be provided containing particulars of that receipt challan.

16. Recording of daily receipts.- (1) The Union Secretary shall maintain the record of dally receipts on the receipt register in Form- AR12.

(2) The receipt challan along with the bank scroll shall be checked for accuracy of the figures, sorted by receipt heads and summed up; and, the error, if any, shall be communicated for correction to the bank through a bank advice.

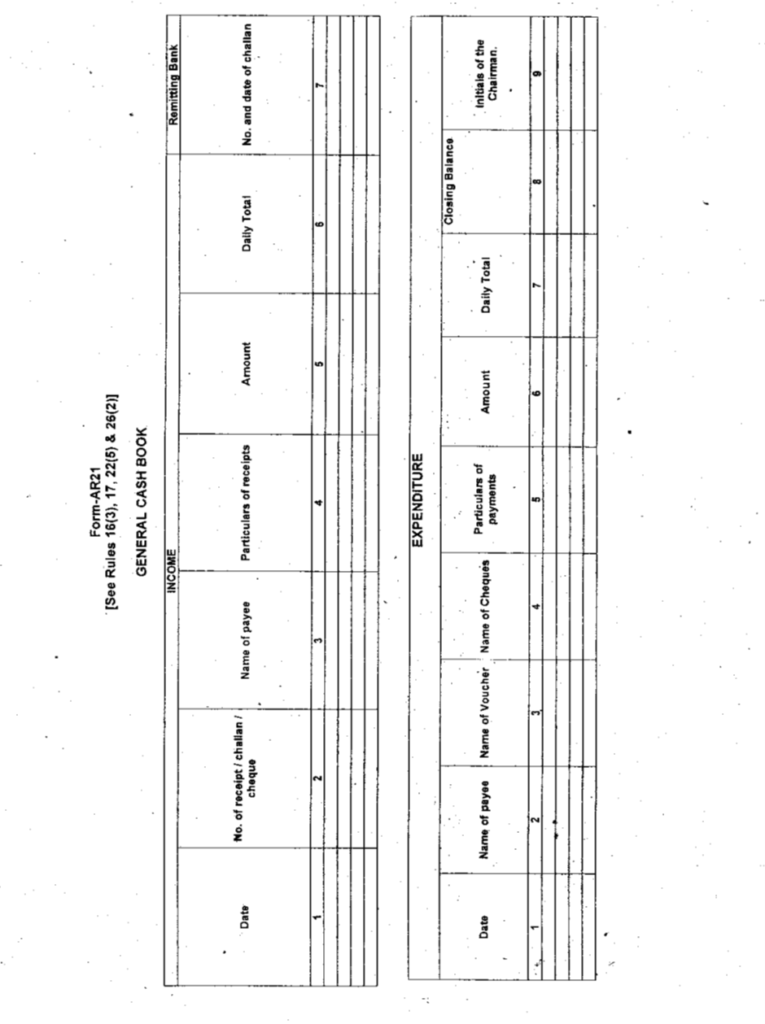

(3) The daily totals for each receipt shall be posted in the general cash book in Form-AR21 at the end of each day.

17. Fiscal transfers. The Union Secretary shall record the fiscal transfers, local receipts and grants from the Government and other agencies in the respective receipt head In Form-AR12 and post them in general cash book in Form-AR21.

PART-V

Expenditures

18. General.- (1) The Union Secretary and Chairman shall ensure the implementation of following requirements in all expenditure transactions:

(a) sanction of all expenditure by the Chairman after observing all codal formalities;

(b) availability of funds under relevant object;

(c) purchase order or agreement;

(d) claim voucher and invoice of the claimant; (e) preparation of claim voucher for payment;

(f) pre-audit of claims and authorization of payment;

(g) issuance of cheques for payment;

(h) recording expenditure in the accounting records;

(i) reconciliation of the daily totals as per daily advice note prepared from the cheque register, with the daily expenditures recorded in the Abstract;

(j) reconciliation of expenditure as per daily advice note with the bank scroll; and

(k) reconciliation of expenditure as per daily advice note and the Abstract with the cashbook;

(2) The Union Secretary and Chairman shall ensure that:

(a) no payment is made:

(i) for a charge which has not been duly sanctioned or which has not been provided in the schedule of authorized expenditure; and

(ii) directly from the cash received for credit to the local fund;

(b) no cheque is drawn or en-cashed except for Immediate disbursement;

(c) no withdrawal or disbursement of money is made unless it is pre-audited by the Union Secretary;

(d) no payment is made unless the claim has validity accrued.

(3) In incurring and authorizing expenditure, the following principles of financial proprietary shall be observed by the Chairman:

(a) exercise the same vigilance in the expenditure from the local fund as a person of ordinary prudence would exercise in respect of his own money;

(b) not sanction any expenditure which is more than the occasion demands;

(c) not approve any expenditure which is directly or indirectly to his own advantage; and

(d) not incur any expenditure for the benefit of a particular person or persons to the disadvantage of the people.

19. Recognition of expenditure.- (1) The expenditure shall be recognized in following manner:

(a) in case, payment is made by cheque, the expenditure shall be recognized and recorded in the accounts of the union council on the date the cheque is issued;

(b) in case payments are made through transfer, the expenditure shall be recognized on the date the transfer is made by the transferor;

(c) in case payments are made from the imprest the expenditure shall be recognized when the claim vouchers are submitted and imprest account is recouped; and

(d) the financial year to which any payment is charged shall be determined by the date on which a cheque or payment advice is issued.

20. Purchase order. (1) A purchase order shall be raised for all contingent expenditures, excluding salaries and utilities.

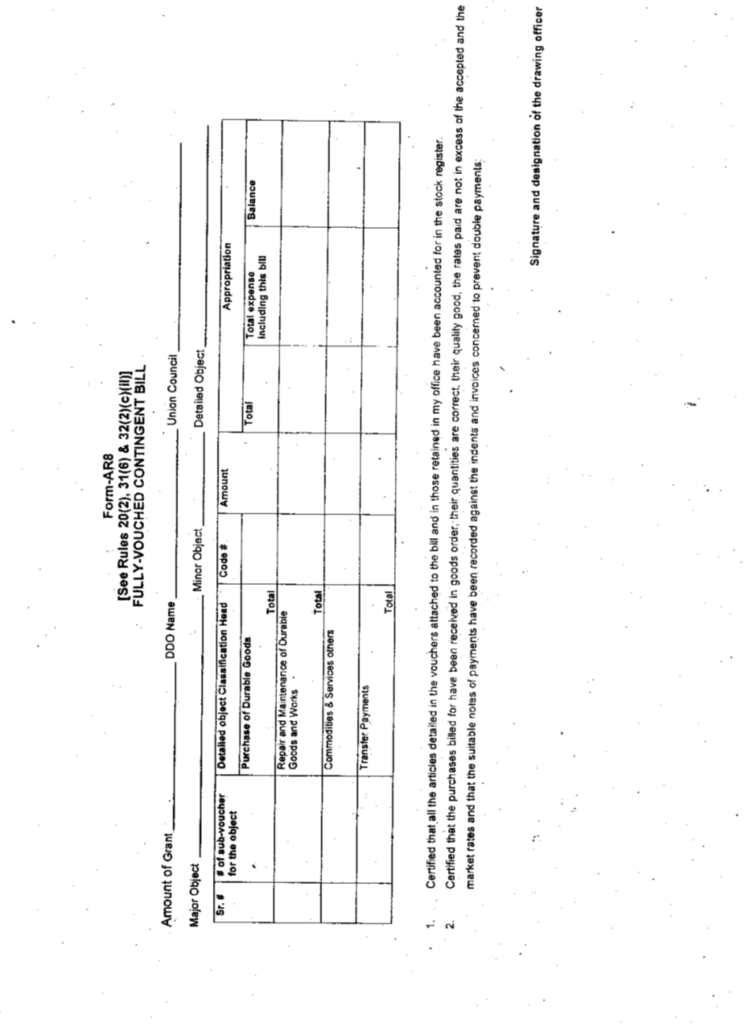

(2) A claim voucher shall be prepared in Form-AR8.

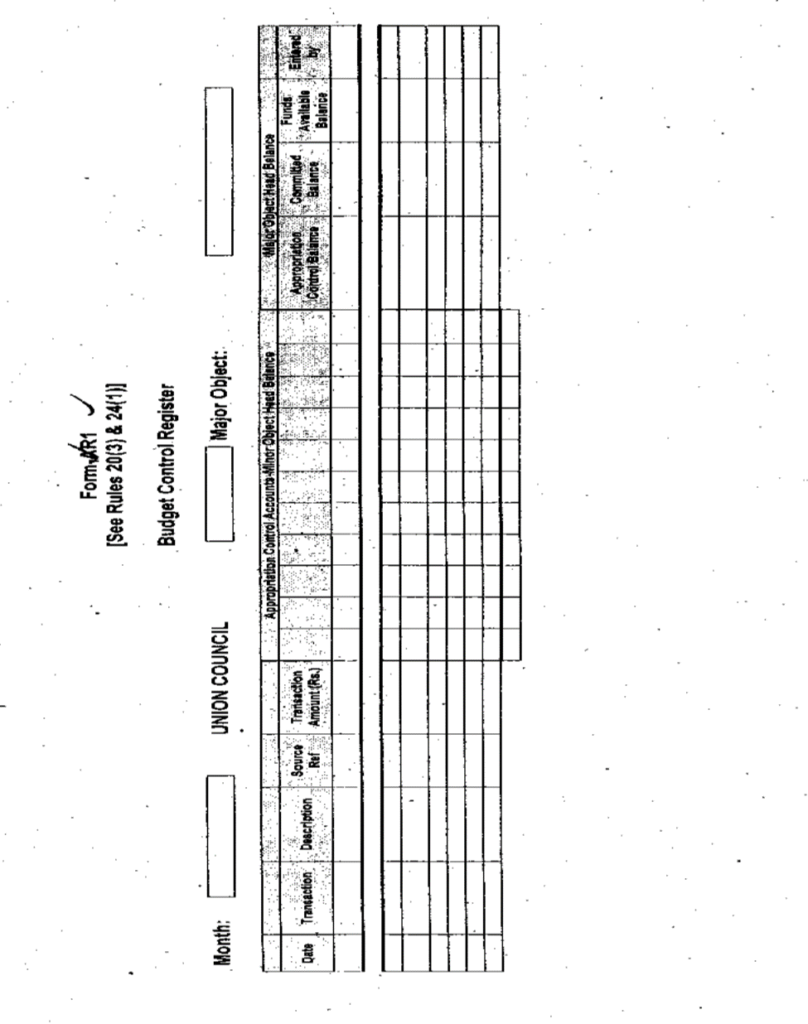

(3) The nomenclature of the budget head to which payment is charged shall be entered in the budget control register in Form-AR1.

(4) For payments in respect of contracts for buildings, works and services, the full amount of the contract and amount of progressive payments shall be supported by certificates and valid payments issued by the Union Secretary and the Chairman.

(5) The deductions, such as withholding tax, security and recoveries shall be set off against the payment due.

(6) The Union Secretary and Chairman making the claim shall provide a statement that the supplies have been received in good order and condition according to the standard specifications and have been entered in the assets or stock register or the services have been satisfactorily carried out according to the standard specifications as provided for in the contract or purchase order.

21. Sanction of expenditure.- The Chairman, as sanctioning authority, shall:

(a) review the claim voucher and all relevant supporting documents, Including the authorized purchase order;

(b) put his signature with the official stamp on the claim voucher for sanction of the claim for payment;

(c) ensure that the head of account to which the voucher is to be charged is correct and is recorded on the face of each voucher; and

(d) ensure that the service has been rendered or supply has been made or works have been executed.

22. Pre-audit of expenditure.- (1) The Union Secretary, while pre-auditing the payments, shall ensure that:

(a) the claims submitted for pre-audit are valid claims on the basis of certificates that the work has been actually executed at site in accordance with the specifications and agreed quantity, service has been rendered to the entire satisfaction of the union council and supply of goods has been made in accordance with the agreed quality and quantity and there is no reason to believe that the claims shall not be paid;

(b) the claim voucher is complete and duly sanctioned and signed by the Chairman with official stamp;

(c) the supporting documents, allied registers and books of accounts such as measurement book, stock register, establishment check register have been attached, verified and are in order;

(d) the claim has not been previously paid;

(e) all the requisite formalities have been completed; and

(f) the claim indicates object of expenditure and there is an adequate allocation for the purpose.

(2) The pre-audit function includes the detailed scrutiny of the claim voucher to guard against possible fraud or irregularities.

(3) If the Union Secretary is satisfied with the claim, he shall authorize the payment.

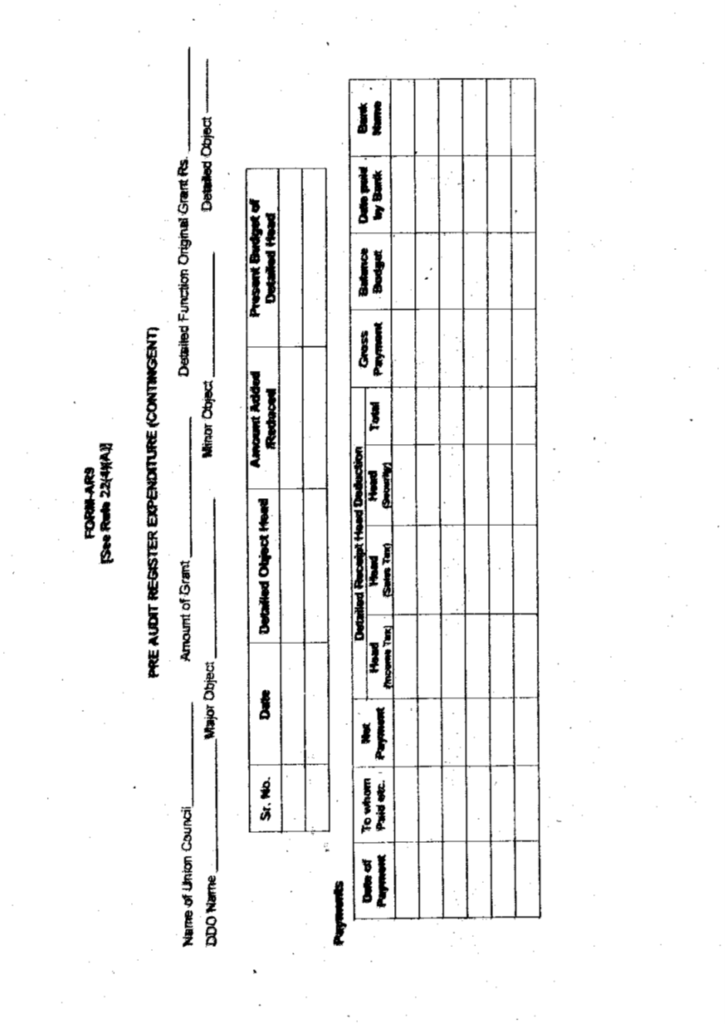

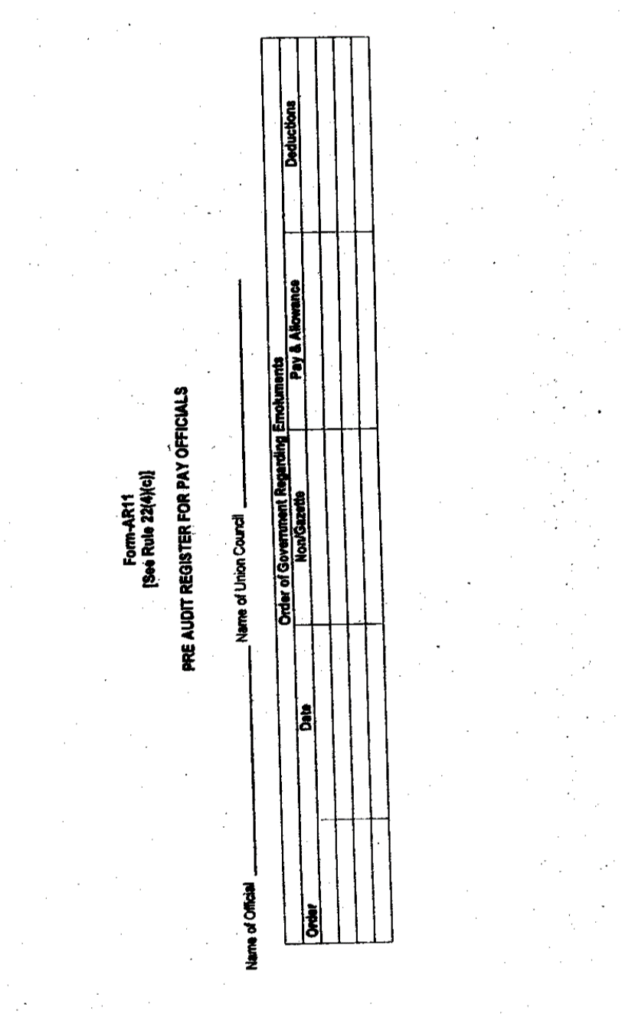

(4) The pre-audit register shall be maintained as follows:

(a) Form-AR9, for contingent expenditure (current);

(b) Form-AR10, for development expenditure; and

(c) Form-AR11, for pay of officials.

(5) All type of daily expenditure shall be recorded in general cash book in Form-AR21.

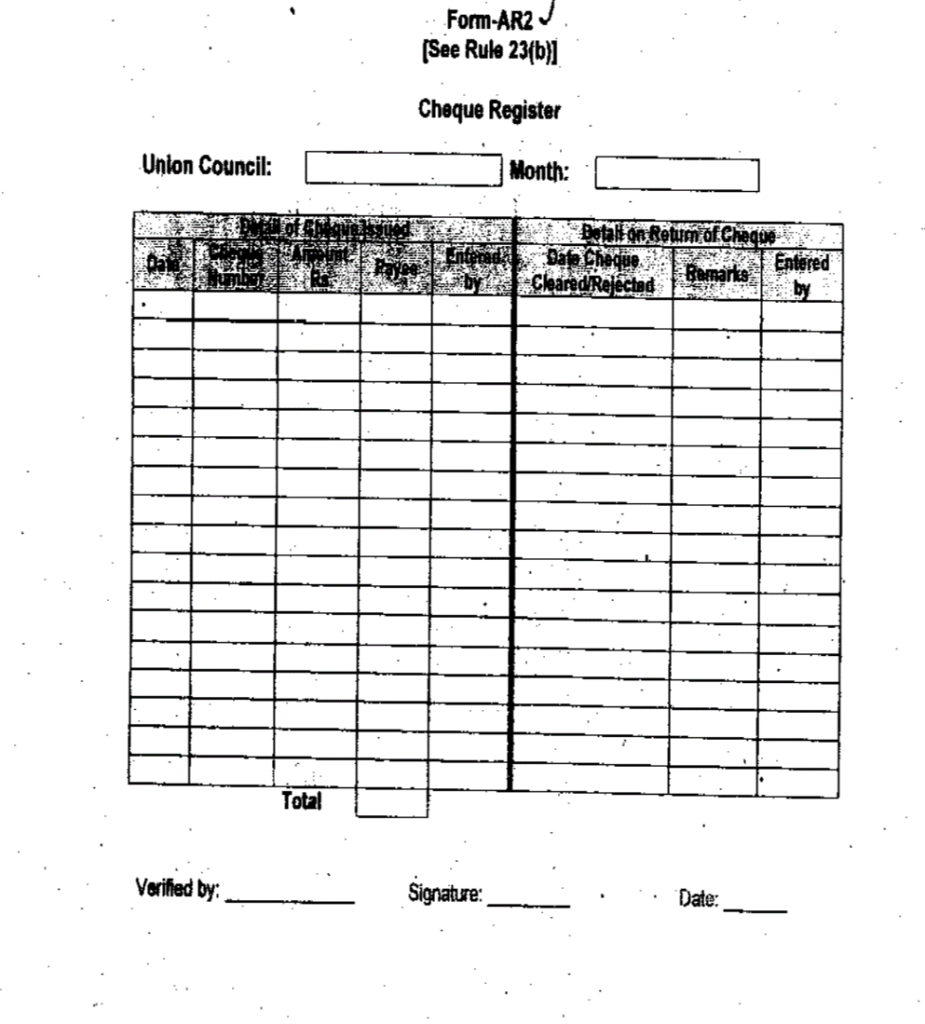

23. Delivery of cheque.- The Union Secretary shall:

(a) prepare the cheque, sign it and submit to the Chairman for signature; and

(b) the cheque shall be prepared and entered in the cheque register in Form-AR2.

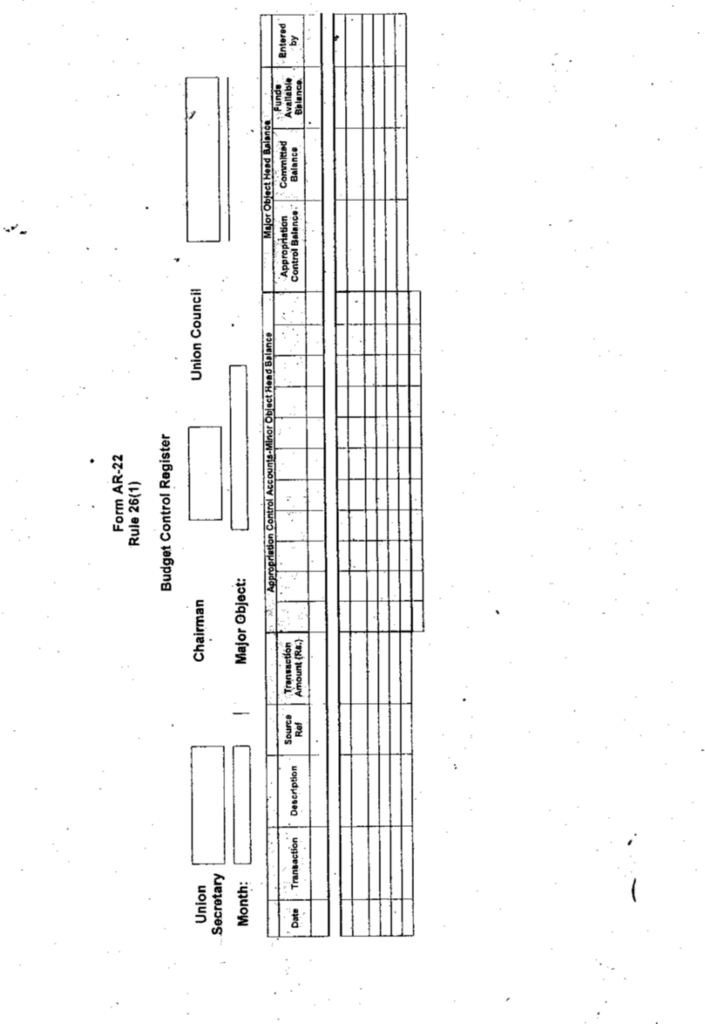

24. Budget control register:- (1) The Union Secretary shall maintain the budget control register in Form-AR1 for purposes of controlling of budgetary allocation and monitoring utilization.

(2) The allocation or residual funds available under each object code shall be recorded in relation to each expenditure transaction in the appropriation control register.

(3) The initials of the head shall be made against the date of payment of each item and the rules regarding the preparation of vouchers shall be carefully observed, and the expenditure shall not cause any excess over the amount provided for the purpose.

(4) The Union Secretary shall take steps to obtain additional appropriation, if the original appropriation is not sufficient.

(5) The payments once made shall be entered in the appropriation control register with the date, name of payee, number of sub-vouchers, the amount and any explanation, essentially required.

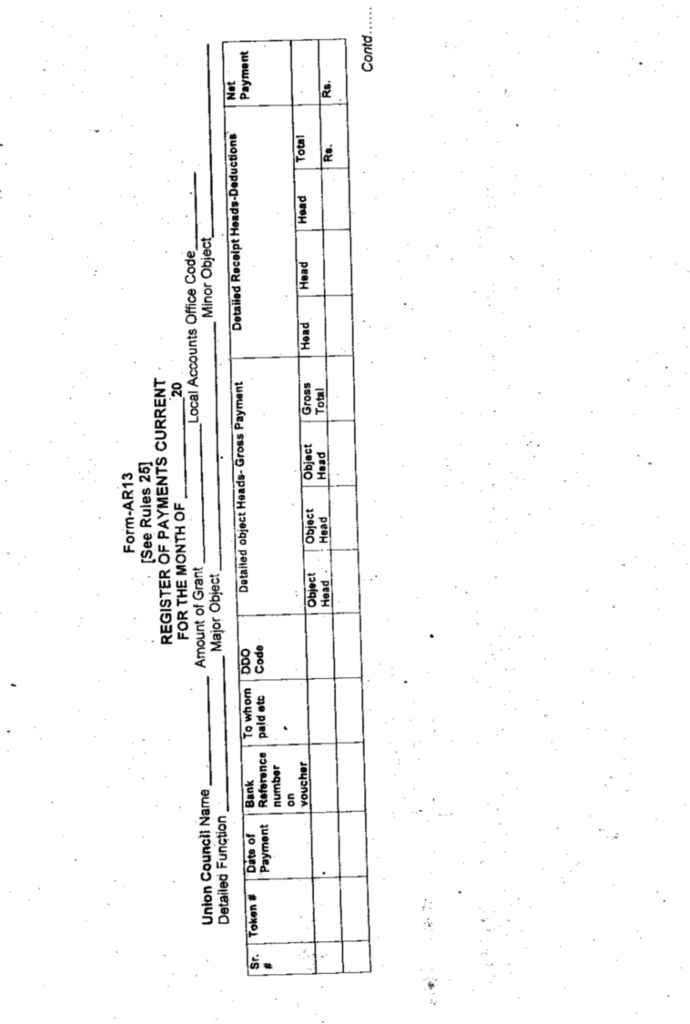

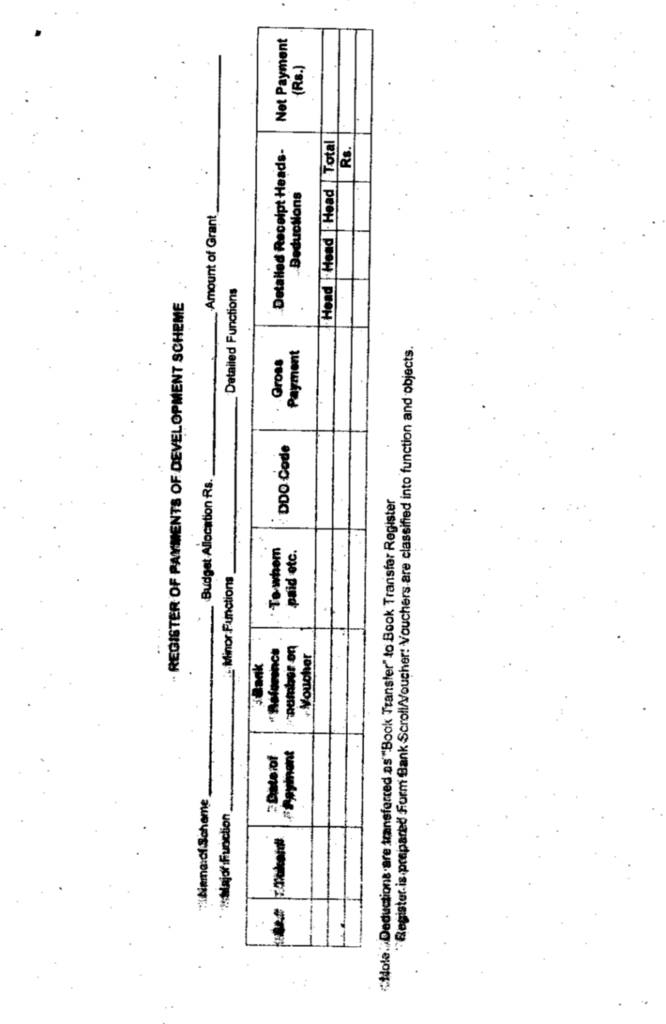

25. Payments register.- The payments pertaining to current expenditure and development expenditure shall be recorded in Form- AR13.

26. Recording of daily expenditure.- (1) The drawing and disbursing officer shall maintain the budget control register in FORM- AR22 for appropriation control and monitoring utilization.

(2) The Union Secretary shall maintain a general cashbook in Form-AR21 for recording the amount received or disbursed on behalf of the union council.

27. Responsibility in payments. The responsibility for payments shall be as under:

(a) besides the responsibilities already determined under Part-III of the rules, it is the duty of the Union Secretary and the Chairman to ensure, on their own part that the claims submitted for payment are valid claims for the works actually executed at site in accordance with the specification and agreed quantity, service actually rendered, as per agreement and to the entire satisfaction of the Union council and supply of goods actually has been made in accordance with the agreed quality and quantity and has duly entered in the relevant books or register of accounts and there is no reason to believe that the payment shall be stop; and

(b) the certificate to that effect shall be essentially recorded on the claim voucher for payment and pre- audit.

28. Reconciliation with the bank.- (1) At the end of each month, the Union Secretary shall prepare a reconciliation statement for reconciliation of expenditure payments with the bank.

(2) After reconciliation with the bank returns, the details shall be cross-checked with the cheque register and the issuance of the cheques by the union council and cleared by the bank.

(3) A report of such reconciliation shall be prepared by indicating the cheques not yet cleared by the bank.

PART-VI

Procedures for Certain Payments

29. Pay, allowances and pension. (1) Except as otherwise authorized by the Government, the salary of the employees of the union council shall not be drawn before the first working day of the next month.

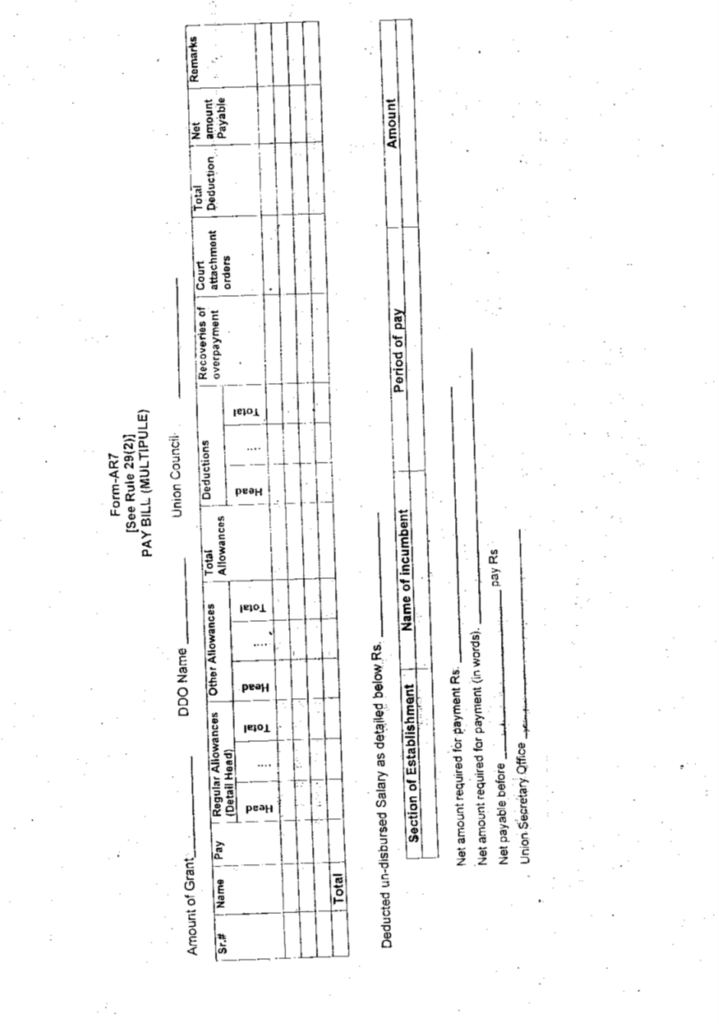

(2) The pay of the establishment shall be drawn in the prescribed Form-AR6 for pay of individual official and Form-AR7 for pay for more than one official.

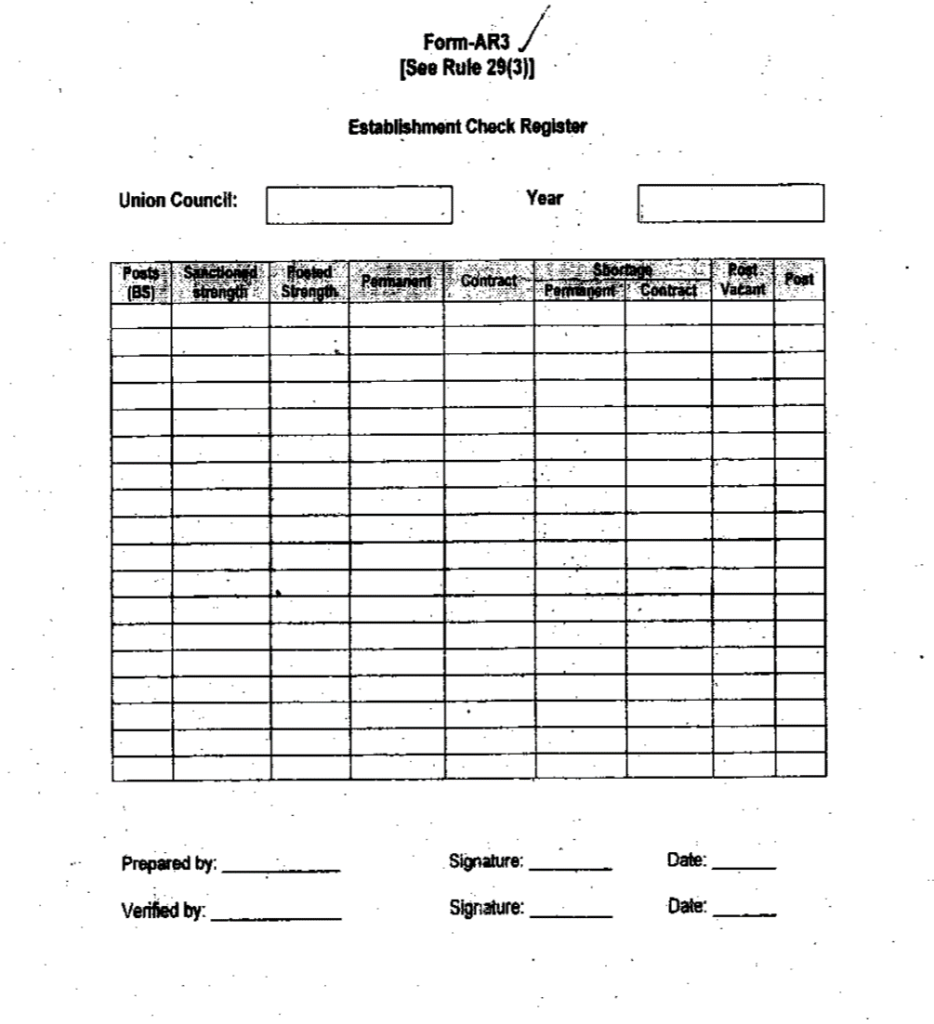

(3) The Union Secretary shall maintain the establishment check register in Form-AR3.

(4) At the beginning of each year, the entries in the establishment check register showing sanctioned strength of establishment of the union council and remuneration for each post shall be scrutinized and verified by the Union Secretary, and countersigned by the Chairman against the relevant entries in accordance with the schedule of establishment sanctioned by the authority competent to sanction it.

(5) Any variation in the schedule of establishment, during the currency of the year, shall essentially require verification by the Chairman.

(6) The Union Secretary shall personally scrutinize and cross check the establishment bill with the establishment check register and sign order of the payment at the foot of the bill in token of correctness of the bill.

(7) The employees of the union council shall be paid, as far as possible, by cheque.

(8) In case of cash payment, the pay of the establishment shall be disbursed, in the presence of Union Secretary, and the signature or thumb-impression of each recipient along with CNIC number shall be recorded opposite his name in the column provided for the purpose in the bill.

(9) The pay and allowances can be drawn up to the day an employee dies and the hour of death shall have no relevance.

(10) In case of payment by bill:

(a) the drawing and disbursement officer shall check the pay bills and verify the total amount entered and Initialed by the Chairman but failure to observe the precautions in any financial matter shall render him liable for making good any loss; and

(b) the Chairman shall be personally responsible for every pay drawn on a bill signed by him or on his behalf until he has paid it to the person entitled to receive it and obtained his receipt, duly stamped where necessary, on the office copy of the pay bill.

(11) In case of payment of salary by cheque:

(a) it shall be handed over to the employee concerned against proper acknowledgement; and

(b) the words ‘paid by cheque’ along with number and date of the cheque shall be recorded on the bill.

(12) In case the payment is made by cash, the bill shall be stamped “Pald in Cash”.

30. Fund and other deductions.- (1) The Union Secretary shall deduct any subscriptions due from pay bills of the employees of the union council.

(2) The deductions from pay bills shall be made strictly in accordance with the rules.

31. Permanent advance.- (1) The union council may sanction permanent advances or imprest to cover petty expenditure up to rupees five thousand.

(2) The payment of an amount not exceeding rupees one thousand may be made from the permanent advance.

(3) The accounts of the permanent advance shall be separately maintained by the Union Secretary.

(4) All vouchers relating to the expenditure from the permanent advance shall be assigned serial number which shall be entered in the permanent advance account register.

(5) In case of low balance, the permanent advance may be recouped through a bill.

(6) The original vouchers must be produced to support the claim for recoupment in Form-AR8.

(7) The imprest account shall always be balanced at any point In time and summed up on the basis of all valid petty cash vouchers to ensure that the amount left in the Imprest account is equal to the value of the imprest.

(8) In the case of payments made from imprest, the expenditure shall be recognized on submission of the claim vouchers and recouping of the imprest account.

32. Payment for works. (1) No payment for works shall be made until:

(a) administrative approval has been obtained from the authority competent in each case;

(b) technical sanction of the detailed design and estimates has been accorded by the authority;

(c) funds to cover the expenditure during the year have been provided in the budget; and

(d) the Union Secretary and Chairman shall ensure that:

(i) the claims submitted for payment are valid claims for the works actually executed at site in accordance with the specification and agreed quantity, service actually rendered to the entire satisfaction of the Union council and supply of goods actually made in accordance with the agreed quality and quantity and entered in the relevant books or register of accounts and there is no reason to stop the payment;

(ii) the certificates to that effect shall be recorded on the claim voucher for payment as evidence for pre-audit purpose.

(2) The following internal controls shall be observed in processing of works:

(a) all bills shall be signed by the contractor;

(b) all bills shall be signed by the engineer or sub- engineer concerned;

(c) the engineer and sub-engineer concerned shall ensure that:

(i) the claims submitted for payment are valid claims for the works actually executed at site In accordance with the specification and agreed quantity, service actually rendered to the entire satisfaction of the Union council and supply of goods actually made in accordance with the agreed quality and quantity and entered in the relevant books or register of accounts and there is no reason to stop the payment;

(ii) the certificate to that effect shall be essentially recorded on the claim voucher in Form-AR8 for the pre-audit purpose;

(d) supporting documents accompanying the bill are valid, duly authenticated and signed by the relevant officer;

(e) the claim has not been previously paid;

(f) the head of expenditure to which the amount is chargeable has been mentioned; and

(g) the funds are available to pay the bill.

33. Refunds.- (1) The revenue paid and credited to the local fund or public account shall be refunded with the approval of the Chairman.

(2) The sanction may be accorded on the voucher itself.

(3) The refund shall be made against the original credit in the union council record.

(4) The refund shall be treated either as expenditure and be paid against approved budget head or adjusted against the income of the relevant head.

Explanation:

(i) if a refund against the local fund relates to a previous financial year, it shall be recognized as an expense in the current financial year;

(ii) where a refund against the local fund is paid in the same financial year, It shall be recorded as a reduction to the relevant receipt head; and

(iii) the refund against public account shall be adjusted against its corresponding receipts.

Part-VII

Monthly and Annual Accounts

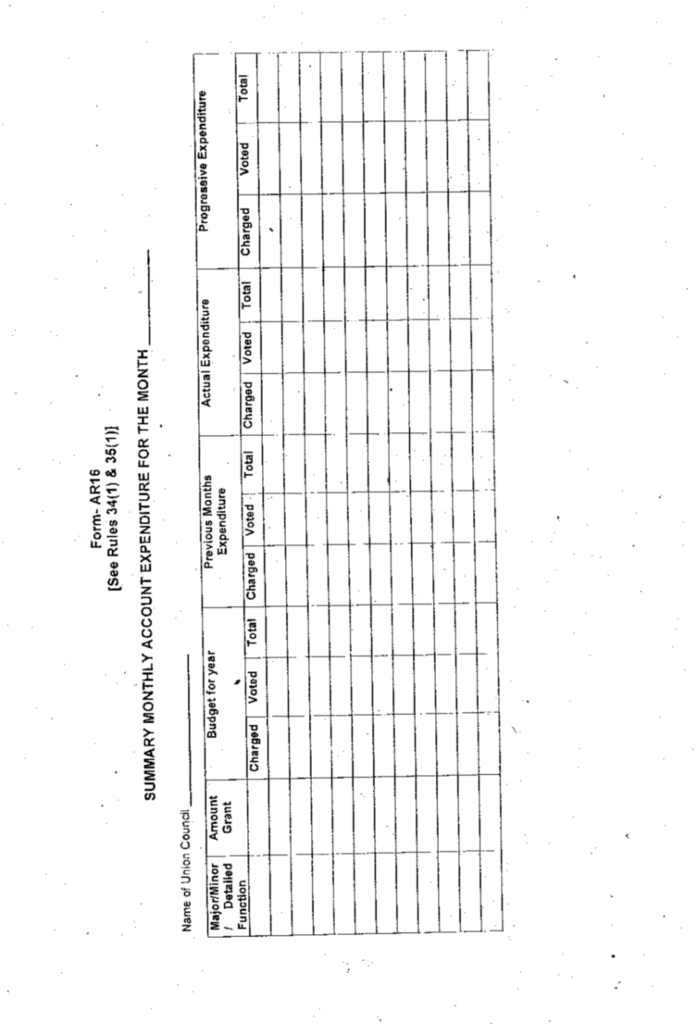

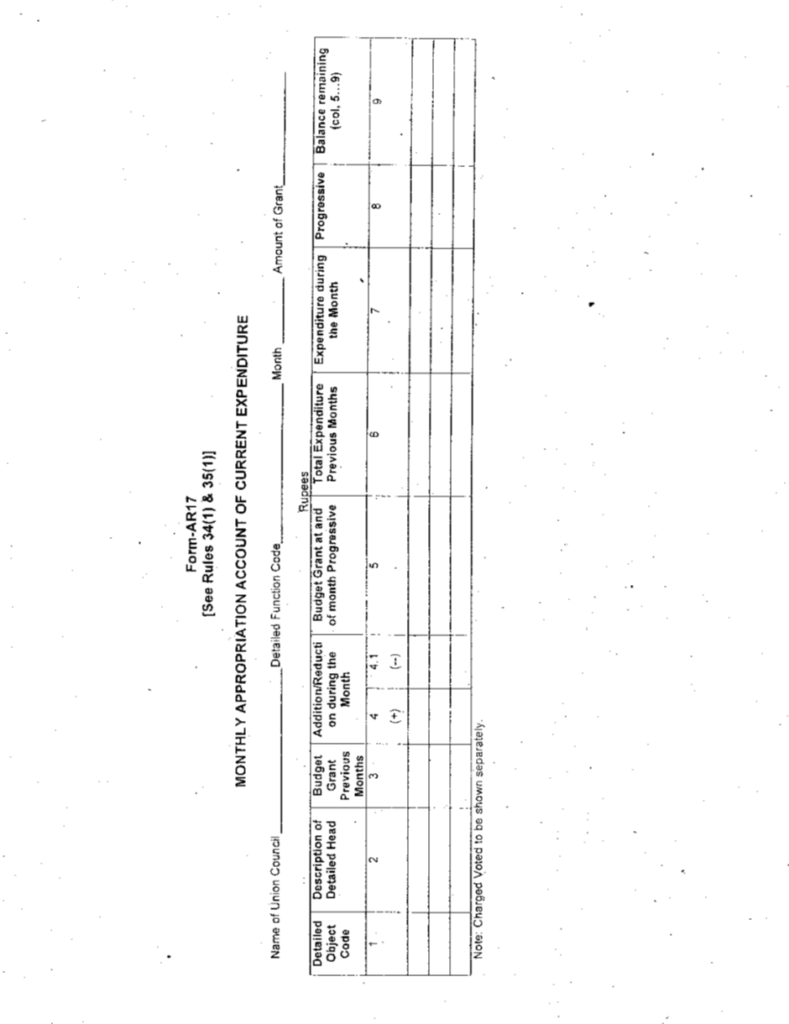

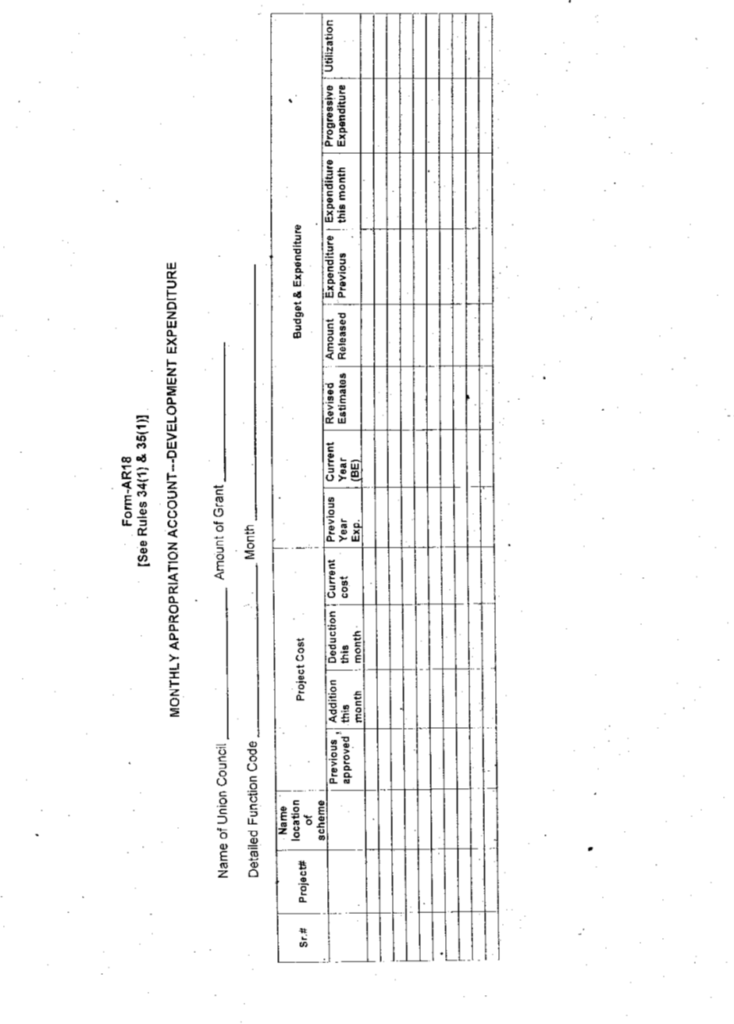

34. Monthly closing of accounts. (1) At the end of each month, Form-ARIS, Form-AR16, Form-AR17 and Form AR18 and the Chairman shall countersign the accounts.

(2) The closing of the accounts for a month shall be the last date of the month.

(3) The monthly accounts shall be prepared by the 10th of the following month.

35. Annual closing of accounts.- (1) At the end of each year, the accounts of the union council shall be compiled in Form-AR14, Form-AR15, Form-AR16, Form-AR17 and Form-AR18 and countersigned by Chairman.

(2) The accounts of each year shall be closed on June 30th and adjustment for the outgoing financial year shall be permitted.

(3) At the close of the financial year, the balances contained in the accounts for expenditures and receipts shall stand closed.

(4) The statement of annual accounts shall be supported by a certificate signed by the Chairman on the basis of the bank statement showing the amount at the credit of the union council in the bank.

(5) The statement of annual accounts of the union council for the preceding financial year shall be submitted in Form-AR14 to the House and the Government by 15th day of July each year.

PART-VIII

Accounts and Audit

36. Display of annual accounts. (1) Annual Statement of Accounts of the union council shall be displayed at a conspicuous place for public inspection, together with a public notice for inviting objections and suggestions containing specific date and time for hearing of the objections.

(2) The House shall examine the annual accounts of the union council consider public objections and suggestions on annual statement of accounts and take appropriate action.

(3) The reconciled statement of annual accounts shall be submitted by the Chairman to the Government by 15th July each year.

37. Annual audit of accounts.- (1) Auditor General of Pakistan shall:

(a) certify the accounts of the union council for each financial year; and

(b) conduct audit of the accounts of the union council in such form and manner as he may deem appropriate. The Provincial Director, Local Fund Audit or any other Audit Agency may, on the direction of the Government, conduct special audit of the accounts of the union council.

38. Annual and special Inspection of accounts.- Punjab Local Government Commission shall conduct:

(a) annual and special inspections of the union council;

(b) special audit of the accounts of the union council, on the direction of the Government; and

(c) social and performance audit of the union council.

39. Audit objections.- (1) The audit paras contained in the Auditor General’s Audit Report shall be considered by the Public Accounts Committee.

(2) The advance paras or the paras proposed for conversion Into draft audit paras and ordinary audit observations contained in the audit and inspection report shall be discussed in the Departmental Accounts Committee or, as the case may be, Special Departmental Accounts Committee.

(3) The procedural Irregularities contained in the audit reports may be regularized by the Government at the instance of the accounts committee, after necessary inquiry that no financial loss is involved in the para and Public Accounts Committee or the Special Departmental Accounts Committee or Departmental Accounts Committee has recommended for its regularization.

(4) Any public loss, if established, shall be recovered from the person responsible or be written-off or waived in accordance with law.

PART-IX

Miscellaneous

40. Interpretation of the rules. In case of any ambiguity or inconsistency arising in the interpretation of provisions of the rules, the decision of the Government shall be final.

FORMS